House Joint Resolution 192 (HJR-192), passed by the U.S. Congress on June 5, 1933, is one of the most misunderstood pieces of legislation in American financial history. Here’s what it actually did — and what it did not do:

Background

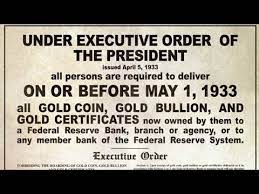

Before 1933, most debts and contracts in the U.S. could be demanded in gold (a “gold clause”), meaning the creditor could require payment in gold coin rather than paper money. During the Great Depression, President Franklin D. Roosevelt took the U.S. off the domestic gold standard and made it illegal for citizens to own most forms of gold coin or bullion.

To support that move, Congress passed HJR-192, which suspended the gold clause in all contracts—public and private.

The Actual Legal Effect

HJR-192:

- Abolished “gold clauses” — It declared that any clause in a contract requiring payment “in gold or a particular kind of coin or currency” was against public policy and therefore void.

- Example: If a contract said “Payable in 20 ounces of gold,” the debtor could instead discharge the obligation in lawful money (U.S. currency).

- Required all debts to be payable in legal tender — Creditors had to accept U.S. paper currency (Federal Reserve Notes or U.S. Notes) for the satisfaction of debts, even if the contract specified gold.

- Protected debtors from default — Since citizens could no longer legally possess gold, Congress ensured they could not be found in breach of contract for failing to pay in gold.

What It Did Not Do

Contrary to many later interpretations:

- It did not eliminate all debt or make debts automatically “prepaid.”

- It did not create a government “trust account” or “credit fund” that citizens can access.

- It did not authorize individuals to discharge debts using bonds, birth certificates, or UCC filings.

- It did not make all money debt-free; rather, it confirmed that all money in circulation was fiat (not redeemable in gold).

Supreme Court Validation

The “Gold Clause Cases” (1935) — Norman v. Baltimore & Ohio R.R., Perry v. United States, and Nortz v. United States — upheld HJR-192.

The Court ruled that:

- Congress had constitutional power to regulate money and void gold clauses.

- Debtors who paid in legal tender fulfilled their obligations.

Summary

In short:

HJR-192 protected citizens from defaulting on gold-based contracts after gold ownership was restricted. It replaced gold-backed debt payments with payments in lawful U.S. currency.

It was a move toward a pure fiat monetary system, where the dollar’s value is declared by the government rather than redeemable in precious metal.

1. The Original 1933 Context — The Removal of Gold and the Birth of Fiat Money

When Congress passed HJR-192, it removed the requirement that debts be paid in gold and replaced all “lawful money” with fiat paper notes—Federal Reserve Notes—declared to be legal tender for all debts, public and private.

This meant:

- Citizens could no longer demand payment in gold.

- The government essentially took control of all “money of account.”

In the public’s perception, this meant the people’s substance (gold) was taken, and in its place, they were forced to operate on credit instruments (paper promises to pay).

2. The “Hidden Trust” Interpretation Emerged (1940s–1970s)

Later theorists—especially after the 1971 closure of the gold window under Nixon—reasoned that if the government took away lawful money (gold), it owed something back to the people.

The logic went like this:

“If we can no longer pay our debts in substance (gold or silver), then every obligation we incur is already prepaid because the government pledged the credit of the people as collateral for the national debt.”

That interpretation grew into the “redemption theory”, which suggests:

- The government created a trust or account (sometimes tied to your birth certificate) representing your share of that pledged national credit.

- The U.S. Treasury or Federal Reserve holds these accounts as surety for all public obligations.

- By “redeeming” or “reclaiming” your status as Secured Party Creditor, you supposedly regain control over that account.

3. The UCC Connection (1980s–1990s)

The Uniform Commercial Code (UCC)—especially Article 9—was adopted nationwide after WWII to standardize commercial law.

Private researchers noticed that:

- The government and courts use the same commercial filing system (UCC) that governs private creditors and debtors.

- Every birth certificate and Social Security Number functions in commerce as a registered entity.

- The “person” named in ALL-CAPS is treated as the debtor, while the living man or woman is the creditor—if properly separated.

They reasoned:

“Since HJR-192 made all obligations payable in credit rather than substance, the government must have already prepaid all public debts. Therefore, by filing a UCC-1 Financing Statement, you can ‘secure’ your position as the creditor instead of the debtor in commerce.”

Thus the Secured Party Creditor process was born.

4. The “Discharge vs. Payment” Distinction

In the redemption framework:

- Payment means extinguishing a debt with substance (gold/silver).

- Discharge means settling it with credit (Federal Reserve Notes, set-off, or bond).

Since HJR-192 abolished gold redemption, all debts are now discharged, not paid—and that’s key to the theory:

“You can discharge obligations because you already contributed the credit (the energy, the labor, the bond).”

Hence, the claim:

- You can issue a “bond,” “bill of exchange,” or “accept for value” to discharge a public debt using your pre-existing credit.

- The government is merely holding the account in trust for you until you act as the authorized agent (Secured Party Creditor).

5. The Core Idea in Private-Commercial Circles

Modern private-commercial theorists interpret HJR-192 as Congress’s admission that no one can pay a debt with substance anymore.

Therefore:

- All debt is an illusion—merely bookkeeping.

- The people’s energy, birth certificates, and signatures fund the system.

- The remedy (hidden in plain sight) is to reclaim your position as creditor by notice, affidavit, and UCC registration.

In short:

HJR-192 is viewed as the commercial cornerstone proving that all “money” is credit and that those who understand the system can operate privately—using bonds, liens, or trust instruments—to offset obligations.

6. The Reality Check

While the commercial interpretation has symbolic and educational value (especially for understanding credit vs. substance and the creditor-debtor dynamic), courts and Treasury do not recognize HJR-192 as creating personal trust accounts or discharge rights via private bonds.

In law, HJR-192 did one thing:

It made all obligations dischargeable in legal tender, removing the gold standard.

In private-commercial study, it became:

The philosophical seed of the “creditor vs. debtor” awakening—a reminder that money is a creature of law, not substance, and that those who understand the law of obligations can operate from the creditor side of commerce.