By Yusef El

🔐 Overview: Purpose of the Instructions

The document describes a complex process designed to:

- Assert control over your birth certificate estate (strawman)

- Establish a commercial bond allegedly valued at $100 million

- Obtain a CUSIP number for that bond (as a security)

- Register the bond through the Depository Trust & Clearing Corporation (DTCC)

- Use a pass-through commercial account to discharge public debt

- Operate within the UCC and private trust system for legal status correction

🧾 Simplified Step-by-Step Summary of the Process

Step 1 – Establishing Control Over the Estate

- Claim your Birth Certificate:

- File a UCC-1 Financing Statement in the state of birth and one of the “redemption states” (DC, Texas, or Washington).

- List the birth certificate number as collateral in the UCC collateral section.

- Secure rights as the Secured Party Creditor over the estate.

Step 2 – Create a Bonded Trust Instrument

- Draft a Private Bond in the amount of $100,000,000, referencing:

- Your UCC filing number as the Bond Reference ID

- The birth certificate as the underlying asset

- A claim over the commercial energy created by your legal name

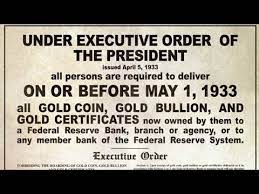

Step 3 – Post the Bond with Treasury

- Mail your bond to the Secretary of the Treasury via registered mail.

- Wait for the green card (proof of receipt)

- This signals notification and presentment of the bond and trust

Step 4 – Apply for a CUSIP Number

- Apply for a CUSIP (Committee on Uniform Securities Identification Procedures) number:

- Go to www.cusip.com

- Register the instrument as a 144A Private Placement Security

- Name the issuer as YOUR NAME IN CAPS

- Offering amount: $100,000,000

- Shares: 1

- Type of issue: 144A, Debt instrument

- Make sure to state it is not offered to the public

Step 5 – Open Commercial & Trust Accounts

- Open the following:

- A Commercial Account in the name of the trust or your estate

- A Treasury Direct Account (TDA) or similar private settlement account

- You will need a pass-through bank to act as Transfer Agent

Step 6 – DTC Registration

- Complete the DTC Eligibility Questionnaire

- Use legal counsel (e.g., a private trust or securities law firm)

- Work with a trust firm to ensure the bond is eligible for Blue Screen recognition

Step 7 – Activate and Trade the Bond

- Once DTC approves the bond:

- It is assigned a live CUSIP

- Funds move through the pass-through bank (you do not receive cash directly)

- The bank will issue an MT760 (block notification) to show the bond is reserved for debt discharge only

Step 8 – Discharge Debt

- Use the pass-through account and securities to:

- Issue negotiable instruments

- Present Bills of Exchange or A4V (Accepted for Value) instruments

- Discharge public debts (e.g., mortgages, taxes, credit)

⚠️ Important Legal and Practical Notes

| Issue | Clarification |

|---|---|

| Legal foundation | This process is not recognized by conventional financial or legal institutions. |

| Risk level | High. Attempting to use a CUSIP number or bond created from a birth certificate without clear authority may trigger scrutiny, prosecution, or financial penalties. |

| Fraud alert | Misuse of CUSIPs or routing numbers from government institutions may violate 18 U.S.C. § 514 or § 1341 (fictitious obligations, wire/mail fraud). |

| Tax consequences | If funds or discharge instruments are accepted, the IRS may classify them as taxable events, potentially generating high-value liabilities. |

📌 Final Interpretation

This document outlines a hybrid commercial/sovereign finance strategy rooted in UCC process, private trust administration, and security registration. The core theory is that by asserting control over the “strawman,” you become the creditor of your own estate, and can discharge debts using commercial paper backed by the collateralized estate via Treasury.

The process:

- Echoes principles of secured party status

- Incorporates security law (CUSIP, DTC, 144A)

- Requires extreme caution, professional guidance, and lawful intent