By Yusef El

In the world of commercial law, a Bill of Exchange is a powerful negotiable instrument governed by the Uniform Commercial Code (UCC), particularly UCC Article 3. It represents an unconditional order in writing, directing one party to pay a specific sum of money to another. But can a private individual lawfully use such an instrument to set off or discharge debt?

Understanding the Legal Basis

A Bill of Exchange is recognized under both domestic and international commercial law. Under UCC §3-104, it qualifies as a negotiable instrument when it:

- Is in writing and signed by the drawer,

- Contains an unconditional order to pay a sum certain,

- Is payable on demand or at a definite time,

- Is payable to order or bearer.

This instrument can be used for discharging debt, but only when the parties involved recognize the obligation, the presentment, and the value of the instrument.

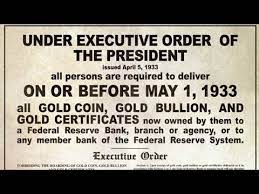

Further, under HJR-192 (June 5, 1933)—passed in response to the removal of gold-backed currency—Americans were no longer required to pay debts in “lawful money.” This created the framework for discharging obligations via offset and credit, rather than payment in specie.

The Supreme Court has acknowledged the lawful use of negotiable instruments:

- United States v. Chase National Bank, 331 U.S. 28 (1947): “Bank deposits are subject to withdrawal by negotiable instruments.”

- Citizens’ Bank v. Parker, 192 U.S. 73 (1904): “A bill of exchange is the representative of money intended to be used as such in the commercial world.”

Setoff vs. Discharge

The setoff process implies a mutual offsetting of liabilities—one debt cancelling out another. In administrative and commercial contexts, a properly executed Bill of Exchange may be used as a tender of setoff, provided:

- There is agreement or acceptance by the opposing party (the creditor),

- The instrument conforms to legal standards of negotiability,

- There is a record of value given or value received.

Practical Obstacles

Despite the legal framework, banks, creditors, and agencies often reject such instruments—not because they are unlawful, but because they operate outside of conventional procedures. The rejection is usually based on:

- Lack of understanding,

- Absence of a pre-existing account agreement recognizing such instruments,

- Institutional policies prohibiting non-fiat tenders.

Conclusion

Yes, the use of a Bill of Exchange to set off debt is lawful—when done correctly and with proper documentation. It must conform to UCC definitions, be issued by a competent party, and be presented with evidence of value. However, without administrative acceptance or legal enforcement, its effect remains theoretical rather than actual.

Those engaging in this practice should pair it with an administrative process (e.g., presentment, notice of default, and affidavit of non-response), and be prepared to litigate or arbitrate if the instrument is dishonored.

If you’re ready to move beyond surface-level knowledge and truly understand how jurisdiction, status, and commercial law intersect, SPC University is where you begin. Our daily webinars, hands-on instruction, and expert-led curriculum are designed to empower you with real tools—not theories—to navigate the public and private with precision. Don’t operate under assumptions—learn to rebut them lawfully. Join SPC University and take control of your legal and commercial standing today.

Disclaimer: This article is for educational purposes only and does not constitute legal advice. Proper use of negotiable instruments in debt discharge requires precision and lawful intent.